Gold’s other-worldly run from 2000 to 2011 was the first ever financial tsunami. What started as a daring concept to eliminate banks and intermediaries has grown into so much more: DeFi 3.0.

This new phase is not merely about decentralisation. Its all about; trust, regulation, real world use and institutional adoption.

In order to make sense of this evolution, I broke down what DeFi 3.0 is, why it’s significant, and how DeFi models are being regulated across behemoth institutions or hybrid —.style platforms shaping tomorrow’s financial landscape.

What Is DeFi? (Quick Recap)

Decentralised Finance (DeFi) is a system where services like lending, borrowing, and trading happen directly between users without banks or intermediaries—fueled by blockchain technology.

Instead of depending on financial institutions, DeFi employs smart contracts, self-executing programs on a blockchain that facilitate transactions automatically and transparently based on rules written in code.

And although this revolution has widened the scope of what is possible, it would be naïve not to acknowledge that all of this has not happened without a hitch.

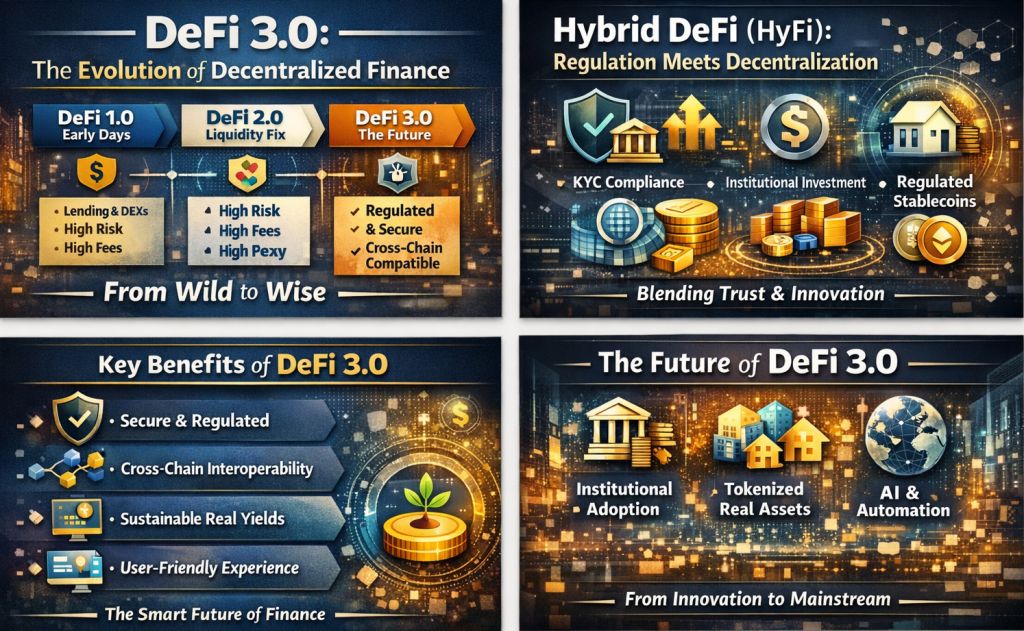

The Progression: DeFi 1.0 → 2.0 → 3.0

✔ DeFi 1.0: The Beginning

- For example, lending and decentralised exchanges (AMMs)

- Potential for High Returns with Risk & Complexity

- Scalability issues and network costs

✔ DeFi 2.0: Fixing Liquidity Issues

- Introduced protocol-owned liquidity

- Attempted to limit reliance on external triggers

- Sustainability and usability remained concerns

✔ DeFi 3.0: The Real Transformation

- There are real-world challenges to be addressed in DeFi 3.0: aspects of security, usability, regulatory uncertainty and adoption.

Unlike DeFi 1.0 and DeFi 2.0 systems, DeFi 3.0 systems are more secure, user-friendly, cross-chain and aware of regulations etc.

Key Features of DeFi 3.0

✔ Cross-Chain Interoperability

DeFi protocols were previously constrained to a single blockchain (e.g., Ethereum).

DeFi 3.0 allows for fluid movement of wealth across networks and builds a global financial system.

This means:

- Lower costs

- Faster transactions

- More liquidity

✔ Security-First Architecture

Let’s be frank, DeFi had a trust issue.

In 2024 alone, hackers and vulnerabilities cost billions.

DeFi 3.0 addresses this with:

- Smart contract audits

- AI-based risk detection

- Decentralized insurance

Real Insight:

I wrote about testing out a DeFi platform during the boom in early 2021. The interface was not straightforward, and one incorrect click might put real money at risk. Today’s DeFi 3.0 apps feel much more like mobile banking apps: streamlined, guided and secure.

✔ Sustainable Yield (Better Than “Too Good to Be True”)

Not long ago, numerous DeFi platforms provided ludicrous and untenable yields.

DeFi 3.0 introduces:

- Real yield from trading fees

- Lending interest

- Tokenised real-world assets (RWAs)

This means long-term stability not just short-term hype.

✔ User-Friendly Experience (UX Revolution)

The feeling around DeFi seemed like a form only developers would find useful.

Now:

Wallets and interfaces have improved, and AI takes decision-making process to a whole new level.

Result: Mass adoption is possible

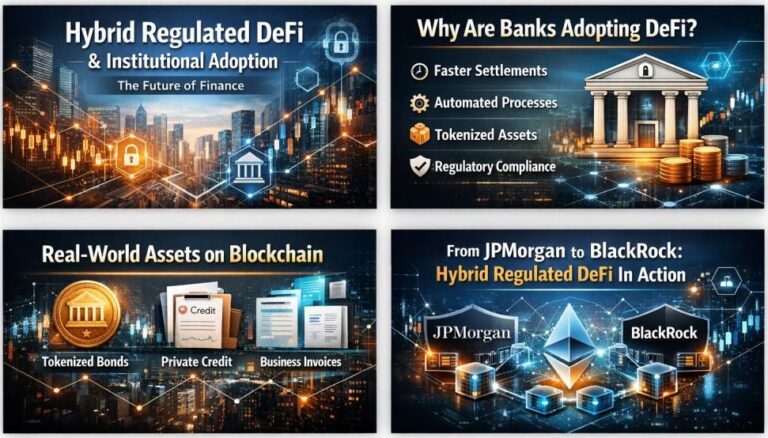

The Emergence of Regulated, Institutional and HyFi

Now we get to the fun part.

✔ The Problem

Traditional DeFi:

- No regulation

- High volatility

- Limited trust from institutions

Traditional finance:

- Highly regulated

- Stable

- But slow and expensive

✔ The Solution: Hybrid DeFi (HyFi)

As we enter the next paradigm, DeFi 3.0, we are seeing the emergence of Hybrid Finance (HyFi)—a balance between decentralised protocols (financial systems operated by code on blockchains with no single body in charge), centralised oversight (traditional regulation and monitoring) and institutional participation (legacy companies entering Dew economy).

This helps limit volatility and improve stability of hybrid systems especially when under market stress (Murphy, 2023).

✔ How Does This Work in Practice?

These include permissioned DeFi pools, KYC requirements for smart contracts or participation, and regulated stablecoins (digital assets at parity with traditional currencies) and bank and government integration.

DeFi 3.0 embraces regulation instead of battling against it.

The Reasons Behind Institutions’ New Interest

For years, major players shunned DeFi. Now they are entering.

Reasons:

- Better compliance tools

- Reduced risk through hybrid models

- Tokenisation of real-world assets (e.g. bonds, real estate)

- Predictable returns

This brings:

- More capital

- More credibility

- More stability

Real-World Example (Experience-Based Insight)

I recently spoke to a fintech founder who told me their company experimented with hybrid DeFi lending.

Initially they were entirely decentralized—but were (insofar as:)

- Trust issues from users

- Regulatory pressure

- Limited funding

After transitioning to a hybrid model with partial adherence and institutional support:

- Investor confidence increased

- Risk reduced significantly

- User growth improved

DeFi 3.0 is all about this: technological innovation, not ideologies.

Challenges DeFi 3.0 Still Faces

DeFi 3.0 holds a lot of promise, but it also is not without fault.

Key Issues:

- Regulatory differences across countries

- Complexity for new users

- Security risks still exist

- Market volatility

DeFi is still evolving and not yet mature.

DeFi 3.0: The Road Ahead (2025 Onwards)

Experts are expecting DeFi 3.0 to bring:

- Onboard millions of new users

- Cross $200 billion total value locked (TVL)

- Integrate deeply with traditional finance

Key Trends to Watch:

- AI-powered financial automation

- Tokenisation of real-world assets

- Integrating CBDCs (Central Bank Digital Currencies)

- Fully compliant DeFi ecosystems

Why DeFi 3.0 Matters to You

Whether you are:

- An investor

- A developer

- A business owner

- DeFi 3.0 enables: enhanced sovereignty, worldwide accessibility, controlled yield and frictionless participation.

In Conclusion: Establishing a Well-Balanced Financial Future

DeFi 3.0: Not Just Replacing Traditional Finance, But Integrating With It

It’s about bringing the best of both worlds together:

- The openness of decentralisation

- The trust of regulation

- The stability of institutions

This balance will bring decelerated finance to the mainstream.

Key Takeaways

- DeFi 3.0: Security, usability and real world adoption

- Instead, hybrid models (HyFi) combine decentralisation with regulation

- Credibility and growth fueled by institutional interest

- The future of finance is not complete decentralisation, but reasoned equilibrium

If DeFi 1.0 was experimentation, and DeFi 2.0 was optimisation, then we’re moving into an era of implementation in DeFi 3.0 — where ideas finally meet reality.